12 dec 2025

Submitting tax returns is a crucial obligation for owners of small businesses. While it may appear daunting, grasping the tax process clearly is essential for your company’s success and financial stability. With tax season approaching, this guide on how to file taxes will be helpful whether you’re doing it for the first time or have been doing that for years.

Before you start filling out your tax forms, make sure you have all the information about your company and your earnings and expenses for the year.

Here’s a checklist of what you’ll need:

To avoid unnecessary audits and tax penalties, it’s crucial not to miss anything. The IRS closely scrutinizes bank records and financial transactions to ensure that every source of income is reported correctly. This includes obvious sources like payments and checks, as well as less obvious ones such as canceled or delayed customer payments, gratuities, prizes, and bartered services.

To keep your records organized and accurate, here are a few tips:

Use software or spreadsheets to track expenses and income. Start with simple tools like Excel if you’re in the early stages of business.

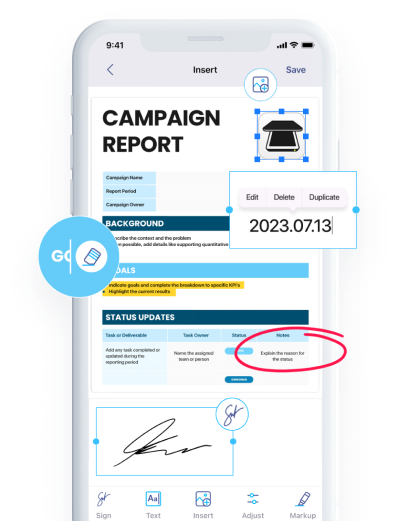

While gathering a year’s worth of receipts can be a hassle, there’s no need to bring all of them to the IRS in a bag. The IRS permits taxpayers to store and file digital documents, as long as the files are easily accessible and can be reproduced without any alteration.

A smart way to track your receipts is by using a mobile scanner app like iScanner. By regularly scanning your receipts for taxes, you can keep everything organized in one place, without the inconvenience of using a bulky scanner. iScanner lets you:

What’s also important is that iScanner takes care of your personal information. All files are stored securely within the app or in cloud storage. If you choose cloud storage, your documents will be hosted on Amazon Web Services, a trusted provider used by most Fortune 500 companies. You can also use the Safe Folder feature to keep all your files there. This type of folder is protected by a PIN.

Here’s a very short instruction on how to quickly scan and keep all your receipts with the help of iScanner:

That’s it. Your receipt is scanned.

Set aside time every few months to review your financial records for accuracy, allowing you to spot mistakes before they become expensive. Good record-keeping not only helps you maximize deductions but also keeps your finances in check, ensuring a smoother tax season.

The next step involves selecting the appropriate tax form according to your business structure. The primary types are sole proprietorship, limited liability company (LLC), partnership (including limited and limited liability), C corporation, and S corporation.

NB! The IRS treats an LLC in different ways depending on how many people own it and what the owners choose. If an LLC has more than one owner, it’s generally classified as a partnership for tax purposes, unless the owners opt to have it treated as a corporation. If only one person owns the LLC, it’s considered part of that owner’s individual tax return, unless the owner opts to have it classified as a corporation.

Sole proprietors should mention their business income and expenses on a Schedule C form and then attach it to their personal tax return (Form 1040). Taxes are then paid according to individual income tax rates.

Sole proprietors with net earnings of $400 or more must also file Schedule SE for self-employment tax.

Both the form and instructions can be found via the link.

After you finish, calculate the net profit or loss to include in your personal tax return.

The IRS offers IRS Free File, a program that allows eligible taxpayers to prepare and file their federal tax returns at no cost using approved partner software. The only requirement is that your Adjusted Gross Income (AGI) is $84,000 or less. If you don’t meet the income requirement, you can still use Free File Fillable Forms, which are free but require you to fill out the tax forms yourself (similar to paper forms, just online).

The IRS Direct File program isn’t available for the 2026 tax year. As a result, small business owners who want to file for free will need to use IRS Free File (if eligible) or third-party tax software. IRS Free File typically opens in January each year, in line with the start of tax season.

If you’re the only owner of the LLC, simply follow the sole proprietor process.

Partnerships and multi-member LLCs follow the same tax filing process. You’ll need to file an information return using Form 1065, along with its instructions, which are available here.

Each partner or member of the company should receive a Schedule K-1 from the accountant, which shows their share of the business’s profit or loss for the year. They then report this amount on their personal tax return and pay the taxes.

While Form 1065 provides the IRS with an overall view of the business’s profits or losses, Schedule K-1 is where each partner reports and pays taxes on their share of the income. You can also download the form directly from the IRS website.

If your business is a C corporation or an LLC taxed as one, you’ll need to file a separate business income tax return using Form 1120 in addition to your personal tax return.

The corporate income tax rate is set at a flat 21%. However, you’ll still face double taxation—first at the corporate level and then again on your personal tax return. Form 1120 is where C corporations can also claim applicable tax deductions.

While Form 1120 is similar to Schedule C, it’s more detailed, complex, and separate from your personal return. The IRS provides instructions for completing it.

If your business is an S corporation or an LLC that has elected S corp status, you’ll need to file a separate corporate tax return using Form 1120S. Shareholders will report their share of the business’s profit or loss on their personal tax return using Schedule K-1. However, the corporation itself must still file its own tax return.

Here’s the form as well as the instructions from the IRS.

They differ based on the form you’re filing.

Form 1065 (partnerships or multi-member LLCs) and Form 1120S (S corporations) are generally due by March 15. Form 1040 for sole proprietors and Form 1120 for C corporations are due by April 15. If the date lands on a weekend or holiday, you should file the form by the next business day.

NB! Filing deadlines depend on the fiscal year your business follows, so it’s important to check the IRS website for accurate due dates.